The humanization trend has accelerated meaningfully, first within pet food, as owners began seeking ingredients they could understand and trust. Grain-free and high-protein formulations emphasizing the absence of artificial preservatives and fillers catalyzed the impressive growth of super-premium categories, such as fresh, freeze-dried and air-dried, often featuring human-grade ingredients.

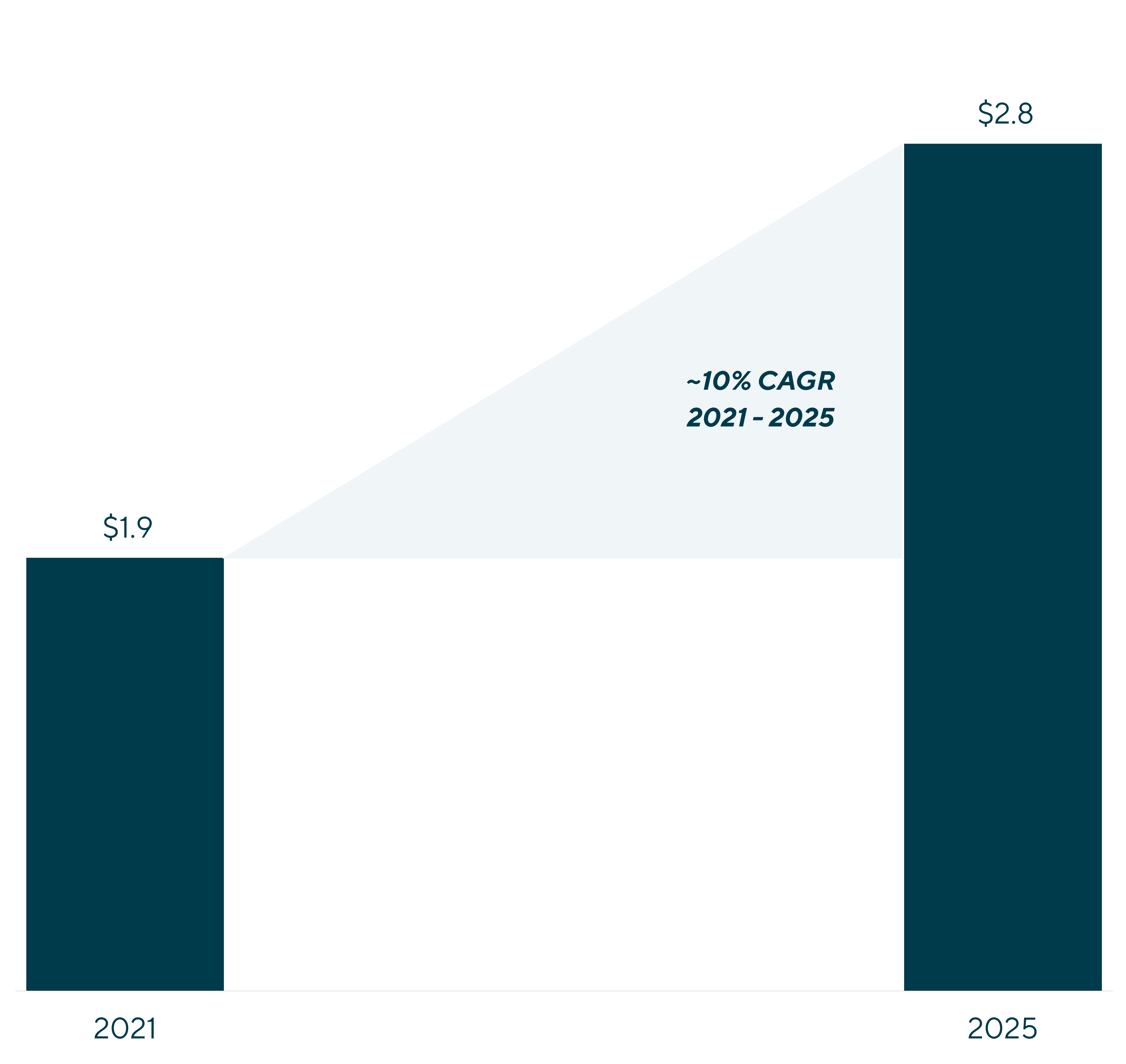

The explosive growth of the pet supplements industry over the past decade clearly demonstrates how the pet industry often mirrors the human world, albeit with a lag. What was once a nascent, vet-dominated category has evolved into a multi-billion-dollar segment and one of the fastest-growing areas within the broader pet industry.

The expansion of these health- and wellness-driven categories is prompting players focused on the treat space to rethink their value proposition. The emerging “snack-with-a-purpose” philosophy bridges nutrition and medicine: rather than offering simple indulgence, treats are increasingly used as a convenient, palatable delivery mechanism for vitamins, probiotics and other wellness needs. As a result, the line between reward and therapeutic supplementation continues to blur, reinforcing premiumization and consumers’ willingness to pay for integrated, proactive health & wellness solutions.

Pet Supplements Market Size

($ in billions)

Functional Applications

Today’s pet parents are looking for treats that address specific physical or cognitive needs, increasingly viewing products as a way to “treat” their pet while simultaneously addressing a health need. The most popular functional areas include:

| Joint & Mobility: Ingredients like glucosamine, chondroitin and omega-3 fatty acids (often from fish or algae oil) are widely used to support aging pets and breeds prone to hip and other joint issues. |

| Digestion & Gut Health: The inclusion of probiotics, prebiotics and fiber-rich pumpkin or beet pulp has skyrocketed to help stabilize the intestinal microbiome. |

| Skin & Coat: Treats enriched with biotin and salmon oil target itching and promote a shiny coat |

| Dental: Modern dental treats frequently incorporate active ingredients like enzymes, zinc or probiotics alongside mechanical abrasion to reduce plaque. |

| Calming & Cognitive Support: Innovative formulations now use L-theanine, valerian root and DHA to help with anxiety and support brain development in puppies or senior pets. |

Current Trends within the Functional Treats Category, Driven by Consumer Demand

|

1 |

Science & Research Validation

Clinical substantiation is becoming one of the most important pillars within pet health and wellness, including functional treats, as pet parents increasingly demand evidence over marketing claims. Brands and manufacturers are increasingly investing in peer-reviewed studies and university partnerships to validate efficacy. Importantly, research is focused not only on ingredient inclusion, but on bioavailability and demonstrable health outcomes. |

|

2 |

Advanced Delivery Formats

Innovation beyond traditional biscuit formats is accelerating, including freeze-dried raw treats, lickable pastes, dual-texture products (e.g., crunchy exterior with soft center) and “squeeze-up” formats that enhance engagement and ease of consumption. Dual-texture and squeeze-up offerings have been particularly important drivers of growth in functional cat treats. |

|

3 |

Gut Health & Microbiome Support

The rise of the “Biotic Trinity” reflects increasing sophistication in digestive health. Formulations are evolving from basic probiotic support to include prebiotics (e.g., non-digestible fibers that nourish beneficial bacteria, pumpkin that supports beneficial gut bacteria) and postbiotics (e.g., inactivated microorganisms that provide health benefits independent of live cultures). This layered approach mirrors advancements seen in the human supplement market. |

|

4 |

Functional Inclusions

Advances in manufacturing capabilities have enabled greater use of visible and embedded inclusions within treat formulations. These inclusions—often functional or sensory—can deliver targeted health benefits, enhance palatability or improve texture, providing both efficacy and consumer-perceived value. |

|

5 |

Ingredient Transparency

Clean-label positioning has evolved from a differentiator to a mandatory trust signal for functional pet treats. Owners increasingly seek recognizable ingredients and clear labeling to avoid additives or allergens. This emphasis on transparency often extends to sourcing narratives, geographic specificity and third-party verification. |

Looking Ahead with LincolnFor investors, the anticipated growth of functional treats is going to create opportunities. Lincoln has worked with numerous pet consumables brands and manufacturers, and we understand the latest market trends and key value drivers. As a result, we can provide timely perspectives on the evolving landscape, adding significant value for both our clients and investors. |

Contributors

Related Perspectives

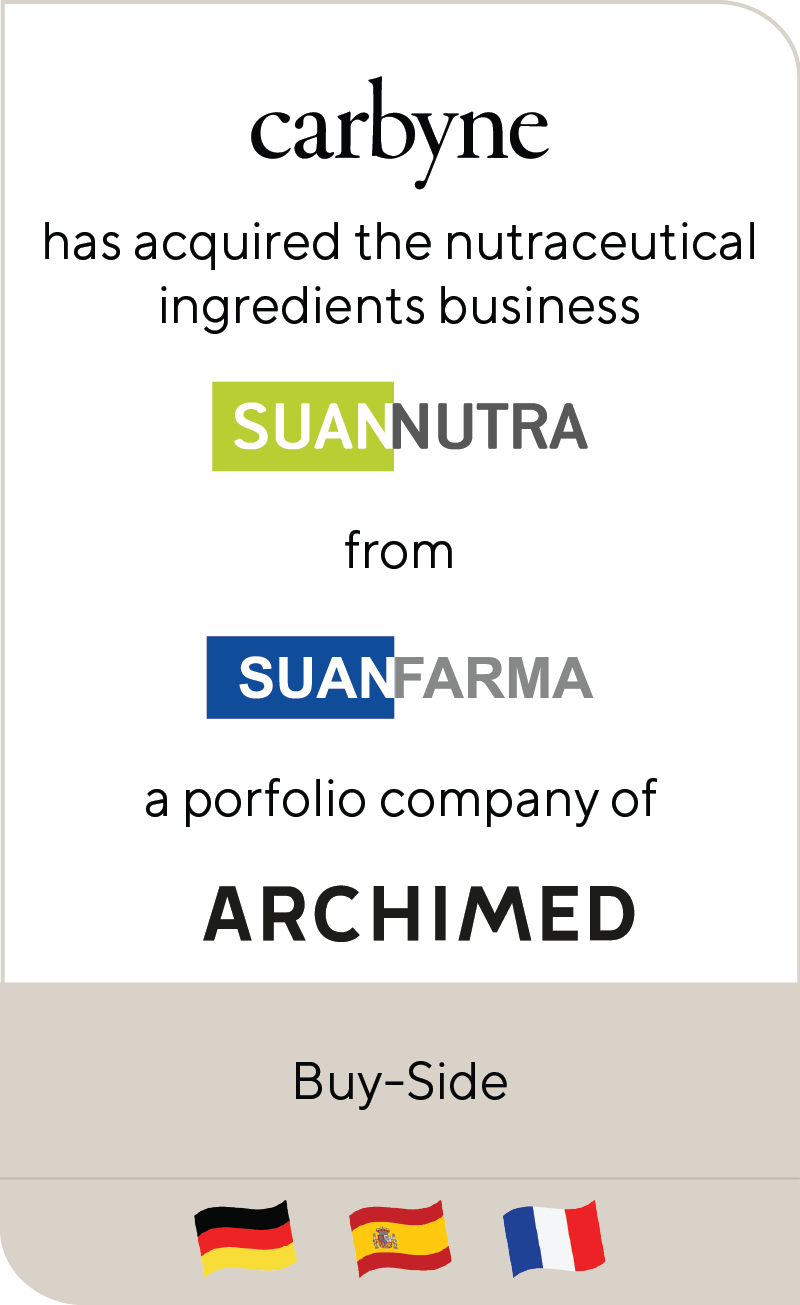

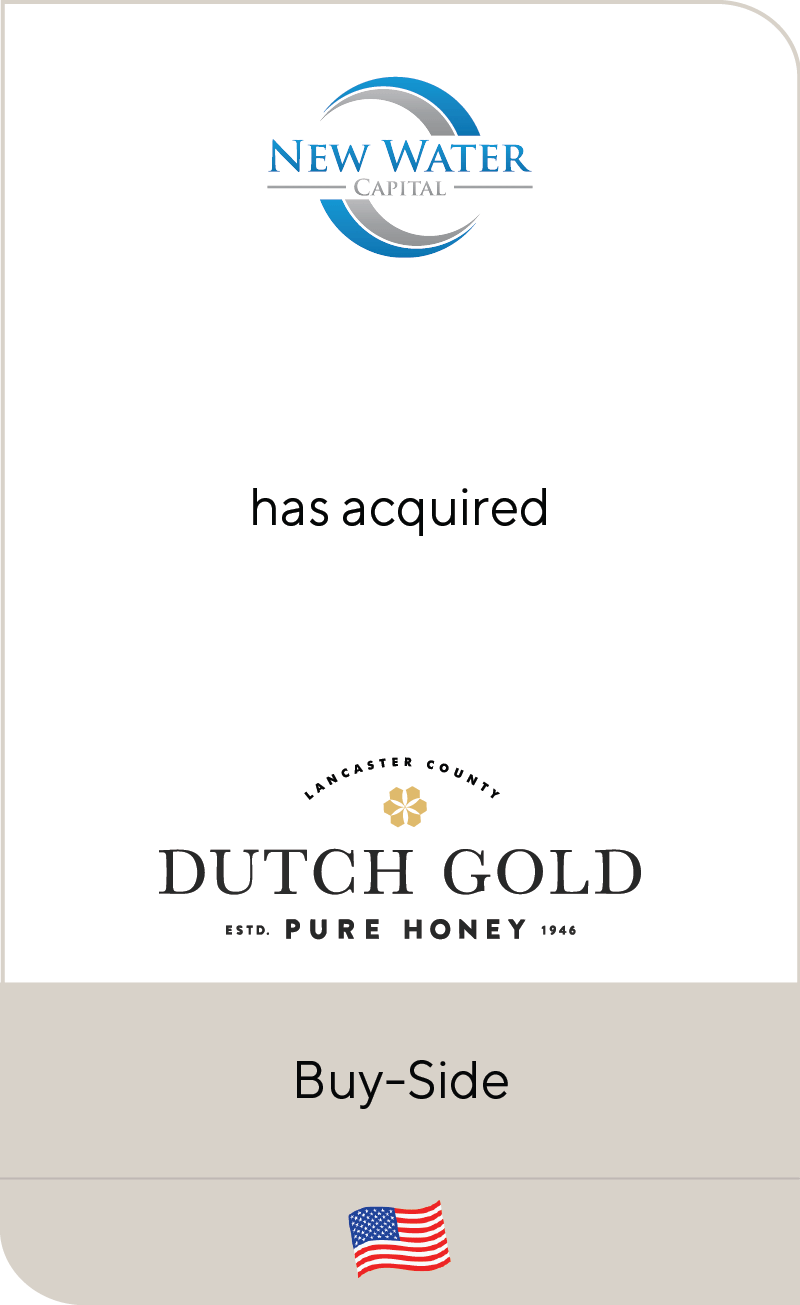

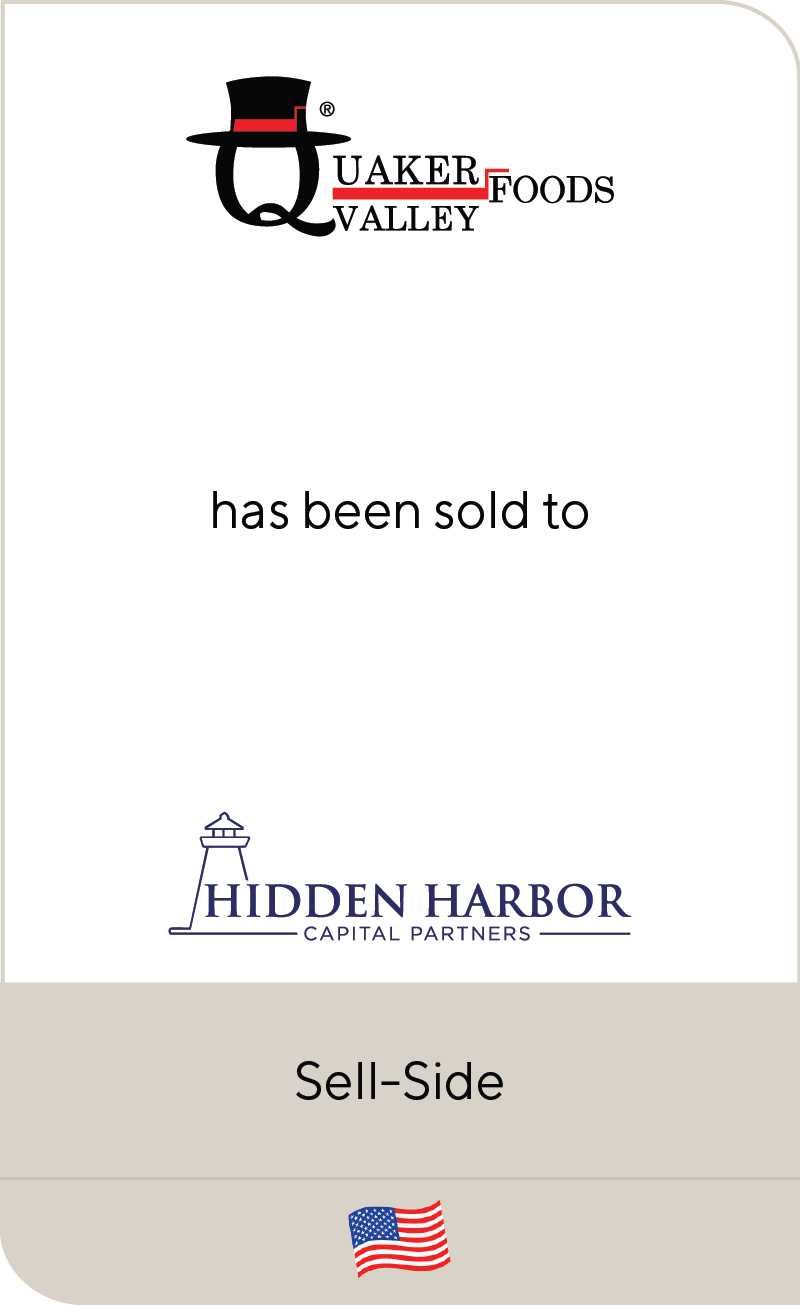

Recent Transactions in Food & Beverage

The Growing Demand for Functional Pet Treats

The global pet industry continues to undergo a significant transformation as the traditional boundaries between food, treats and supplements blur. Once seen as simple rewards or indulgences, dog and cat… Read More about The Growing Demand for Functional Pet Treats

Spotlight on Battery Storage

The global energy landscape is undergoing a profound transformation, and the battery energy storage system (BESS) sector is emerging as a cornerstone of this transition. In this series, Lincoln International… Read More about Spotlight on Battery Storage

Matthew H. Lee

Matt specializes in providing mergers and acquisitions (M&A) advisory services to clients across the technology sector, including private equity firms, private founders and large corporations. Matt has experience with both… Read More about Matthew H. Lee

Andrew Aversa

Andrew provides mergers and acquisitions (M&A) advisory services to clients including domestic and international private equity firms, entrepreneurs and large corporations. He has nearly a decade of advisory experience and… Read More about Andrew Aversa

Lincoln International Adds Kunal Kalra as Managing Director, Expanding Software Coverage in Europe

Lincoln International, a global investment banking advisory firm, is pleased to announce the addition of Kunal Kalra as a Managing Director in its Technology Group. Based in the firm’s London… Read More about Lincoln International Adds Kunal Kalra as Managing Director, Expanding Software Coverage in Europe

Kunal Kalra

Kunal is a Managing Director in Lincoln’s Technology Group and provides mergers and acquisitions (M&A) advisory services to private equity firms, sovereign wealth funds, founders and global corporations. Kunal has… Read More about Kunal Kalra

Data-Driven Value in EMS M&A

No matter the sector or situation, data is often the most important asset in a seller’s toolkit. Still, money is being left on the table and transactions are being put… Read More about Data-Driven Value in EMS M&A

AI in Transport & Logistics: Execution, Neither Hype nor Fear

News and market moves on Feb. 12, 2026 underscored both how AI is already reshaping transport and logistics and how easily investors can overreact to a hint of disruption. Micro-cap… Read More about AI in Transport & Logistics: Execution, Neither Hype nor Fear

European Fire & Life Safety Services Quarterly Review Q4 2025

Looking back at the fourth quarter, the general sentiment in the fire and life safety sector in Europe is that mergers and acquisitions (M&A) activity remains resilient and dynamic, with… Read More about European Fire & Life Safety Services Quarterly Review Q4 2025

Lincoln International Adds Sara Rachele Napolitano as Managing Director

Lincoln International, a global investment banking advisory firm, is pleased to announce the addition of Sara Rachele Napolitano as a Managing Director in its Technology Group. Based in the firm’s… Read More about Lincoln International Adds Sara Rachele Napolitano as Managing Director

Alberto Sanz

As a Vice President in Lincoln’s Industrials Group, Alberto provides mergers and acquisitions (M&A) advisory services to corporates, founders and private equity investors. He has experience advising on complex strategic… Read More about Alberto Sanz

trans.info | High-Quality Transactions Will Shape Transport and Logistics M&A in 2026

Originally published by trans.info on February 20, 2026. The correction phase is over, but rather than a deal boom, discipline and selectivity are shaping the transport and logistics mergers and… Read More about trans.info | High-Quality Transactions Will Shape Transport and Logistics M&A in 2026

AI as a Structural Inflection Point for Tech Services Firms: Implications for CEOs, Private Equity Investors and M&A Processes

Valuations of many listed Tech Services and Software companies have come under pressure, driven by uncertainty around AI’s structural impact on delivery models, pricing power and long-term margin resilience. Harald… Read More about AI as a Structural Inflection Point for Tech Services Firms: Implications for CEOs, Private Equity Investors and M&A Processes

Sara Rachele Napolitano

As a Managing Director in Lincoln International’s Technology Group, Sara Rachele provides mergers and acquisitions (M&A) advisory services to private equity firms and founders. With nearly two decades of advisory… Read More about Sara Rachele Napolitano

VerkehrsRundschau | German Cold Chain Logistics, in Focus

Originally published by VerkehrsRundschau on February 4, 2026. International sponsors and strategic acquirers are increasingly interested in Germany’s refrigerated and frozen food logistics sector, mirroring global growth trends. Recent transactions… Read More about VerkehrsRundschau | German Cold Chain Logistics, in Focus

WealthBriefing | NatWest Scales Up Wealth Ambitions

Originally published by WealthBriefing on February 10, 2026. The NatWest Group’s recent acquisition of Evelyn Partners, valued at $3.69 billion enterprise value, underscores the importance of wealth management to the… Read More about WealthBriefing | NatWest Scales Up Wealth Ambitions

Fashion & Apparel Market Update Q4 2025

In the fourth quarter of 2025, global fashion and apparel mergers and acquisitions (M&A) activity moderated as dealmakers balanced improving medium-term confidence with lingering macro uncertainty and year-end execution constraints.… Read More about Fashion & Apparel Market Update Q4 2025

WSJ | Brookfield Sees More Opportunity Than Threat in AI

Originally published by The Wall Street Journal on February 5, 2026. Despite a multi-day selloff of technology stocks in the public markets, private capital market data shows strong growth and… Read More about WSJ | Brookfield Sees More Opportunity Than Threat in AI

Handelszeitung | Mergers & Acquisitions in Times of Political and Technological Uncertainty

Originally published by The Handelszeitung on January 29, 2026. After years of sluggish growth following the COVID-19 pandemic, Swiss dealmakers have almost gotten used to the continued cadence of major… Read More about Handelszeitung | Mergers & Acquisitions in Times of Political and Technological Uncertainty

2025 Global Results

As we approach Lincoln International’s 30th anniversary in April 2026, we are proud to reflect on the incredible growth we have driven in the global private capital markets. Our success… Read More about 2025 Global Results

Jake West

Jake provides mergers and acquisitions (M&A) advisory services to clients across the technology industry. He has experience advising on and executing both sell-side and buy-side transactions for leading private equity… Read More about Jake West

Mergermarket | TMT Dealmakers Enter 2026 with AI Momentum

Originally published by Mergermarket on January 22, 2026. Dealmakers across the technology sector entered 2026 with optimism, buoyed by a strong end to 2025. Deal volume rose throughout the year,… Read More about Mergermarket | TMT Dealmakers Enter 2026 with AI Momentum

Thomas Collyns

Thomas provides mergers and acquisitions (M&A) advisory services to clients across the aerospace and defense (A&D) sector. His experience includes sell-side and buy-side M&A advisory, corporate divestitures, financings and broader… Read More about Thomas Collyns

Christina Enders

Christina provides mergers and acquisitions (M&A) advisory services to clients across the consumer industry. Her clients include private equity firms, small and medium-sized enterprises, family-owned businesses and large corporates. With… Read More about Christina Enders

Packaging Quarterly Review Q4 2025

Following a subdued 2024 mergers & acquisitions (M&A) market with valuation resets and prolonged political uncertainty, the packaging M&A market experienced a meaningful rebound in 2025.